I got my hands on iDealwine’s 2026 Barometer (thanks to @OrlaithSmith ) — their annual deep dive into the global fine wine auction market — and the Burgundy dominance story is very much intact. Still king globally. Still commanding the highest prices at auction. Still the obsession of collectors from Hong Kong to Germany.

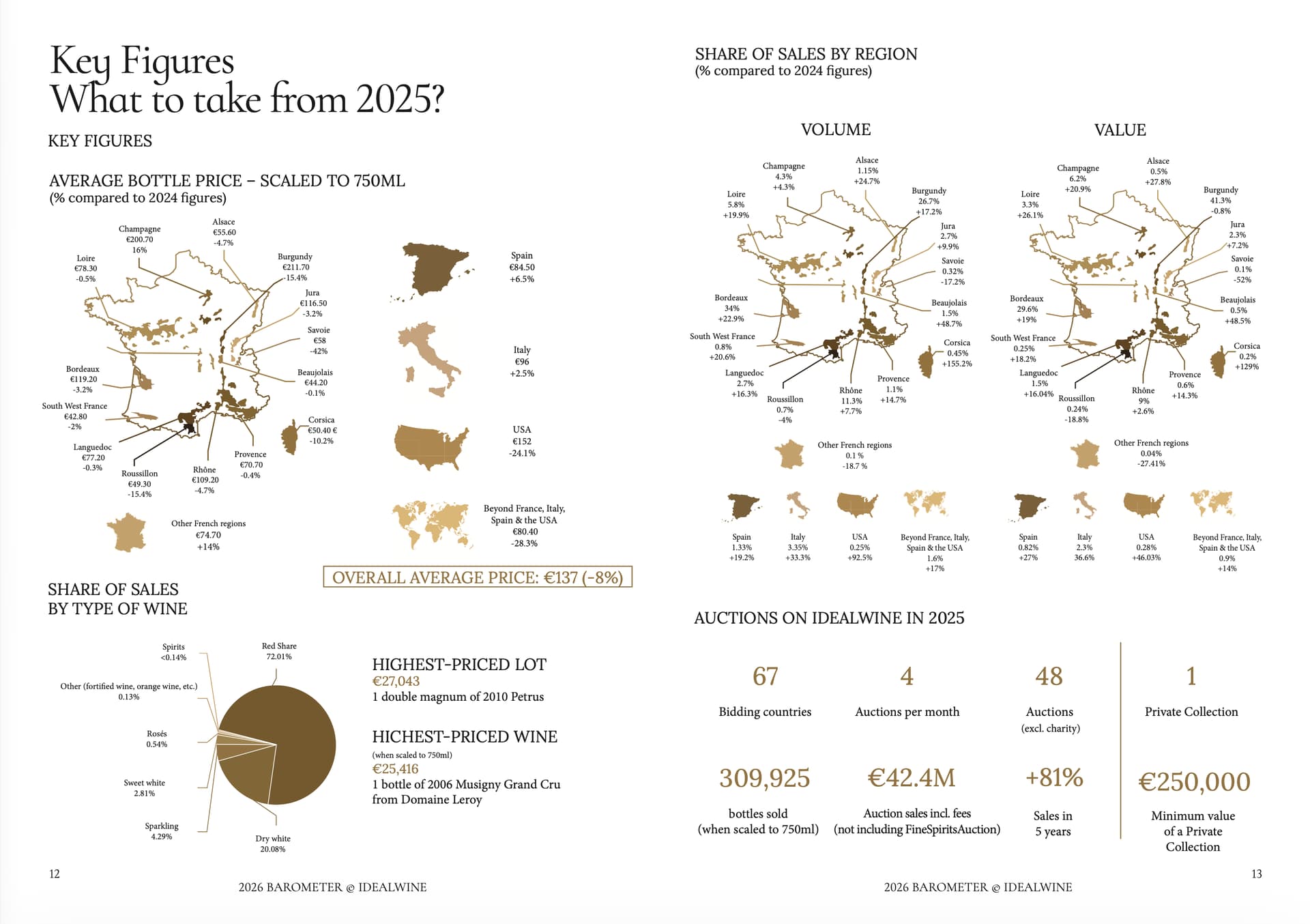

But here’s the thing that jumped out at me: iDealwine had a record year in 2025 — €42.4 million in auction sales, up 9%, with volume up 19%. And within that record year, average Burgundy hammer prices actually softened while Bordeaux quietly gained meaningful ground at auction for the first time in a while. Burgundy still represents over 40% of total auction value, but Bordeaux climbed from 27% to nearly 30%. Not a takeover — not even close — but a real shift worth noting after years of Bordeaux seemingly heading in only one direction.

thanks @ToddFrench - agreed that the data shows we might be entering a new, more positive, era for fine Bordeaux. In general, the secondary market tends to act as a kind of precursor for the wider fine wine sector. Only time will tell but the data doesn’t lie!

To dive a bit deeper into Bordeaux figures: One in three auction bottles is Bordeaux again. The most recent data shows that Bordeaux accounts for 34% of all bottles sold at auction. More striking still, Bordeaux saw auction volumes surge by 23% last year, with 105,000+ bottles (when scaled to 750ml) sold on iDealwine. When looking at total value, Bordeaux sales exceeded the €12.5 million mark, a 19% rise in one year. The average price of Bordeaux wines at auction in 2025 dipped slightly by 3%, less than the overall average of 8%.

When ranking the top twenty Bordeaux properties that are highest in demand among collectors, a handful of properties stood out recording striking increases in their volumes, signalling either a resurgence of interest or strong strategic decisions by well-informed investors. Taking two properties involved in significant appellation and ranking changes in recent years: Château Lafleur and Château Figeac, iDealwine has analysed the auction results. Sales volumes from Château Lafleur doubled in 2025 – its withdrawal from the Pomerol appellation seems to have attracted interest from both collectors and consignors – but the sky was not the limit for bidders and the average hammer price dropped to €471 (-25%). At Château Figeac meanwhile, there was a sharp rise in the volume (+72%) sold at auction with only a marginal dip in average price (-3%), confirming the momentum and enduring appeal of this property since its elevation to Premier Grand Cru status.

Looking beyond the First Growths and the top 20 ranked Bordeaux châteaux at auction, several properties have recorded a particularly sharp growth in value, namely Vieux Château Certan (+141%), Château Canon (+112%), Château Rauzan-Ségla (+91%) and Château Smith Haut Lafitte (+88%). These performances point to a broader re-evaluation of highly sought-after names among bidders. In terms of average price, Château Le Pin stands sits just behind Petrus with €2,417 at the top of the auction rankings, nicely illustrating the premium consistently awarded to micro-estates in the Pomerol appellation.

I can have a look at top Burgundy in the report too, if it’s of interest?

Bordeaux value increase compared to 2024 figures (19%) is driven by a volume increase over the same time period (22.9%). So, Bordeaux has become more popular to sell, but is actually losing value per unit.

Times are tough and people are cashing-out; in conjunction with this – lucky for the sellers – ongoing tariffs make now a good time to sell at auction. These two factors help explain increased volume.

Interesting thread and I appreciate the data from @OrlaithSmith above. Tracking UK exchange activity (via WineStreet) in this quarter vs last, there has definitely been an uptick in transaction volumes. While bids and offers have remained broadly flat on exchanges (with the exception of some labels), when wines do transact, they do so at a higher price, suggesting the floor is rising. Perhaps buyers growing frustration with en primeur, combined with a broader narrative of wine market optimism is heightening activity?

Good points - I’m not sure what effect US tariffs have had, since I don’t know what the US market share is of Bordeaux sales, but I’m guessing it isn’t sizeable, in quantity at least.

I suspect that there is a big difference between the health of the trophy wine market and the rest of Bordeaux.

I’m a regular iDealwine buyer and occasional seller, and I haven’t noticed any upturn in prices of the wines I’m interested in, my “market” being mainly 20€ to 80€). In this category, prices flatlined several years ago. To illustrate this, I’ll take two examples from the 2016 vintage, which could reasonably be seen as the type of vintage which would normally be driving any resurgence in Bordeaux sales:

Sociando-Mallet: no real change since 2021. Can be had for 38€, commission included, roughly equivalent to the original EP price.

Giscours: at 63€, no change since at least 2019 and the same price as EP.

The interesting detail is the lack of increase post-EP. This is the case for practically all Bordeaux barring the trophy wines, at least concerning iDealwine. I would say that iDealwine is one of the reasons for the inexorable and IMO irreversible decline of EP. There is literally no point in buying EP when you can buy at the same price, and often less, after release, with the added advantage of having read in-bottle reports. Indeed, you can even buy a bottle and taste it yourself before committing to a case. What is quite ironic is that iDealwine now provide an EP service themselves!

The increase of quantity doesn’t surprise me at all. Bordeaux has enjoyed an unbroken run of at least decent vintages since 2014, with three of four outstanding ones - that’s a huge amount of wine to sell, a lot of which pops up at auction. I don’t know what the Bordeaux market share of iDealwine is in France, but it must have greatly increased over the last ten years. With the increase of prices and the change of taste, midrange Bordeaux have almost disappeared from French hypermarkets - so for aficonados iDealwine provides a useful service.

I found your discussion of the impact of recent vintages of interest. My sense has been that in the recent past, the most heralded vintages like 2005, 2009 and 2010 were more of a minefield than have been more recent vintages. Some of this was probably due to Parkerization of wines hitting extreme temperatures but whatever the cause, some wines that were really lauded early have not aged well. Certainly, there have been major successes in these vintages, but also major failures. 2005s, for example, have a mixed reputation because of the high failure rate of wines from St. Emilion despite, in my experience, the vintage being pretty consistent in the Medoc.

But contrast, my sense is that the more recent top vintages like 2016 (possibly the best vintage in Bordeaux since 1982), 2019, 2020 and 2022 are more consistent, particularly in the price ranges you prefer. I have drunk a number of 2016s but fewer of the more recent vintages, so a lot of what I am saying is based on what I read but it is also based on what I tasted in Bordeaux when I was there in 2024.

Great vintages build excitement in Bordeaux, always have.

One of the interesting changes in Bordeaux in recent years IMHO has been the revival of the wines from the appellation of Margaux. When I was first buying Bordeaux in the 1980s, with a few exceptions (Margaux, Palmer, Rauzan Segla and a few others) the wines from there had a reputation of underachieving. Now, a lot of wineries from there are making attractive wines where the prices have not caught up with the prices for wines from Pauillac and St. Julien, esp. in your price range. Don’t know that this has anything to do with the changes in auction markets, but still this is an interesting change.

It’s true now, but we didn’t know at the time! But I agree that recent vintages are more consistent, as you say. Particularly in comparison to 2005, they benefit from the improvements in winemaking. Tannins are better managed, are much finer and less imposing than before, rendering the wines much more enjoyable at an early age. Greater accessibility along with greater freshness must contribute to their appeal.

Margaux - it’s very true that quality has improved generally, and that this is where the value is today. There are a huge number of châteaux, not just the CCs, producing good wines at the right prices.

US market - I’ve read the full report, which doesn’t make clear what the US market share of Bordeaux sales is compared to other markets, but it does say that sales to the US dropped by 19% in 2025, due to the tariffs. Of total sales to the US, Bordeaux only represented 16% in volume and 14% in value.

Retail in France - the three older vintages you mention (05, 09 and 10) dealt the EP market in France a series of body blows. 05 in particular destroyed the sense of trust in EP as people like myself were infuriated to see virtually all the wines bought EP sitting on shelves during the annual Foires aux Vins, at discounts ranging from 10 to 25%. iDealwine was only a minor player at the time but as I wrote earlier, they have really taken over since.

You know what? Your post made me realize a key point that I hadn’t previously realized: these are figures from iDealwine, which is not US-based. Therefore, I retract my comments about tariffs. … I’ll just see myself to the back of the room now. LOL!

My best surmise to explain uptick in Bdx. sales is current pricing relative to back vintages sitting out in the marketplace. Bordeaux has done itself no favors with recent pricing, which has the effect of inspiring folks to back-fill, and we all know auction is one of the best ways to do that. Just a thought; no idea the extent to which it’s accurate, however.