wow

1 Like

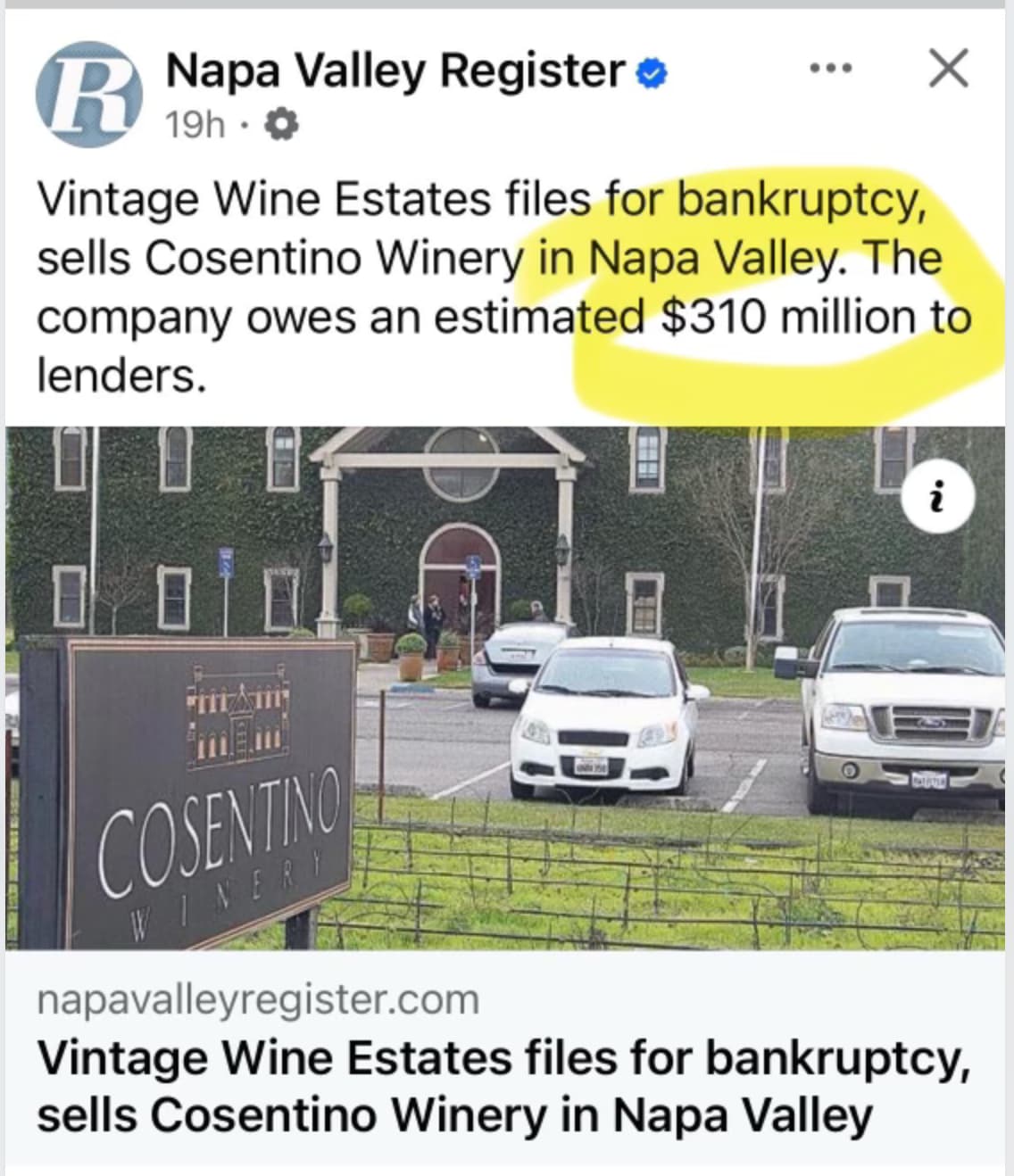

Tell that to Cooley:

btw my comment was just good natured ribbing.

1 Like

Yep - not good . . .

As I said above, I don’t see them dragging themselves out of this and I think they are headed towards Ch 7

Cheers

1 Like

probably too early to say that. Chapter 7 would suggest there is very little value in the portfolio. The lenders will restructure the debt and take some equity. If they could get the business close to cash flow break even and reduce the debt service they might survive.

BTW, why someone with better winemaking intentions never bought Cosentino from just a pure location stand point. I mean, you are literally next to Mustards. Every person that goes to lunch there should be told to go right next door for an after lunch tasting. The wines were never good though.

2 Likes

Is Cameron Hughes (the entity owned by Vintage Wine Estates, not the individual person) the owner of the De Negoce brand? Or is that a different venture that he did which isn’t owned by Vintage?

Cameron Hughes (Vintage Estates) does not own de Negoce (dN). dN was a venture started by Cameron Hughes (the person) and now seems to be owned by Martin Ray in some capacity after Hughes disappeared from the day to day operation of dN about a year ago. dN still markets with with his likeness though.

It’s weird.

3 Likes

Once he starts a new similar wine business again there will be the one with his name, the one with his picture, and then his actual business. It’s like he has clones.

1 Like

Years from now they will compare Cameron Hughes to Pommard and Dijon 777

2 Likes

Aye, this topic is missing some key perspectives about Vintage Wine, and how it got here. I’ll not share the whole shebang, as it might greatly denigrate (ie. piss off) leaders involved. Several key points to note:

-

SPAC Last-chance - as I heard it (from insiders), the SPAC that acquired VWE was a Canadian spac created to acquire/fund a cannabis-based company, but the originators were running out of time (if a SPAC doesn’t use its collective funds within a certain timeframe, they must refund the $$ to their investors. So they “settled” for VWE and took it public. Early prices were $10-$16. Pat Roney and his team made big $$.

-

Public Co Woes - until most wineries, the challenge of being public is quarterly reporting (as well as other regs). Soon VWE’s inventory problems became evident. Then they had to revise previous earnings…and the swirl continued and grew deeper. And the stock kept it’s steady descent down below $2, thus subject to delisting. At one point, I challenged a CFO buddy of mine - the reported assets were $650M, and the market value was only $65M, a stunning 10-1 ratio…his advice - sometimes its best to let sleeping dogs lie…and not with a 10-ft pole.

-

New Mgmt - the Board then hired a new CEO (from LVMH) to remedy…seems like a good guy, hasn’t hired the best team…and the end is clearly in sight.

Too bad - VWE had some solid brands, just suffered from poor management (before the SPAC). After the SPAC, just one problem after another. Poor SPAC investors, they got wiped…

Just one perspective among many…

5 Likes

This is public knowledge. They merged with Bespoke Capital’s SPAC, which was indeed cannabis-focused. A number of the cannabis SPACs of that vintage ended up doing non-cannabis deals, because there simply weren’t any to be had. Kind of like what happened to lots of other SPACs. So Bespoke pivoted to make their spiv, rather than return the public money and lose their investment (I’m guessing a few million the sponsor usually would put up).

Also, delisting is a risk at $1, not $2. They never got delisted, at least not until the bankruptcy filing….

Marc, I stand corrected…thanks for the details. What wasn’t being spoken about were the mgmt faux pas and troubles that sunk VWE…plenty of good brands and actually decent vino - the SCV (Sonoma Coast Vineyards) had some fab wines, as did the other brands.

I am sure you know the risk capital on a $360 mm SPAC is a lot more than a few million. Closer to $10 mm or more. The UW’s get 2% as soon as the SPAC is raised which comes out of the sponsor capital plus all of the other expenses including legal, accounting, insurance.

Out of curiosity I have been digging into this deal. WOW it is really sad. The founder of VWE rolled all of his equity into the deal. I did not check if he sold anything, I am guessing not or not much, so he lost his company and all of his equity. It did look like VWE was on the ropes before they did the SPAC deal, which is odd because that was the best time ever for the wine industry. Their financials showed a company that was overlevered and struggling with liquidity issues. The value of the original VWE shareholder’s equity stake was ~$240mm at closing. Guessing they were hoping to keep the majority of the money in the SPAC as well as the $100 PIPE to properly capitalize the company. They did ok closing the deal with ~$300 mm in cash which is good for SPACs of that era most had closer to 100% redemption.

Post de-SPAC, they did some really odd acquisitions including buying a Somm Company that did virtual tastings and Vinesse a DTC wine company, a Cider company and a Ohio Winery.

The reporting on this has been really terrible. Some articles say they are going to lay off all of their employees, yet the company’s own press release says it will be business as usual during the restructuring process.

BTW one of the Bespoke Capital Partners is a member here. I don’t know if he was directly involved in the deal.

2 Likes

Not to repeat what has already been said, but want to give some further insight as i have been working with VWE for 15 yrs or more. VWE had a philosophy of buying distressed properties for far less value than they would have been in their heyday and running them as brands being produced from a centralized hub winery (buying a winery that might have a production facility, closing it and consolidating production). Anything they bought in Napa became just a front, all production was pulled and moved to Girard winery, anything bought on the Sonoma side they would close and send the production to their ray’s station winery in Hopland (old Fetzer). They bought Tamarack in Walla Walla, let everybody go and sent everything to Owen Roe… However, 7/10 wineries that VWE bought they did not resurrect as had hoped.

Operationally they have a HUGE brand that sucks all their resources called JOSH CELLARS. This was the biggest cash cow for the company (or cash flow provider). They were the producer and operational partner for Josh (owned by Deutsch) and started producing for them when it was 25,000 cases and last year they produced over 6 million cases!!! (all out of the VWE rays station winery in Hopland). Industry rumors are that the new CEO for VWE came in and saw that they were actually dedicating tons of $$ and resources to keep the josh machine going and after more careful review of the partnership with Deutsch realized it was not profitable business and he was keen to either raise prices dramatically to continue producing or cancel the agreement to focus on company owned brands. However, option 2 right now is an uphill battle due to current climate with larger volume brands taking the biggest hit in the current wine market and investment in these brands are needed and …looking at their current financial state, the $$$ needed to invest in these brands is not there.

Edited for case count on Josh - 6 million cases (originally i accidently wrote 3).

8 Likes

I was told that employees were advised yesterday that they indeed are doing a mass layoff.

2 Likes

That is terrible. I don’t know how you preserve value in a business like making wine if you just stop operating. Thanks for all of your color. How bad is this going to be for growers who will be losing grape contracts? I know it is bad but just curious how bad in this current environment.

Interesting, I didn’t know that VWE made Josh. I knew Deutsch were based out of the northeast and thought it weird that they made Josh but figured they just had their own big production facility somewhere. Presumably Josh is larger than all of the VWE brands combined? What does Deutsch do in this situation?

1 Like

This is the genesis of the issue, lots of great wines, but no great brand to anchor the portfolio in NASA retail. It’s always good to have halo brands that fit multiple channels and needs, but without an anchor brand NASA retailers don’t need you or your specialty items.

There was rumors before the SPAC and after they were going to buy Mondavi or Woodbridge which would have provided the NASA anchor.

I hope they get out of bankruptcy as there really are some fabulous wines, but it’s going to take a write down on inventory, repositioning of some brands, and a severe sku rationalization.

1 Like

Wouldn’t Mondavi be way too big? I didn’t look up what they are doing for revenue but did find it was purchased for $1 bn 20 years ago.

CBI was selling off the value brands at the time most of which went to Gallo, like I said rumor only, so I would assume they targeted Woodbridge and much like Gallo, believe they were told both Mondavi and Woodbridge together or no deal.