“And some things that should not have been forgotten were lost”

A highly successful narrative for attracting investments into Fine Wine is to claim it is a safe-haven investment, cushioned from the volatility and downturns of major markets. This logic has always been questionable (Will open a new thread on embedded foreign exchange later). However, Fine Wine has benefited greatly from the 14 year period of nearly zero interest rates globally, and now is suffering from their normalisation. Following Russia’s invasion of Ukraine in 2022, and the resulting spike of inflation leading to higher interest rates, wine prices reversed immediately. Fine Wine, like other non-income generating alternative investments, is highly correlated to interest rates.

This resulting selloff has been the worst market environment for Fine Wine in a generation. The previous correction in 2012-2013 was sharp and focused mainly on top Bordeaux wines. For 2022-2024, it has been wide-spread with prices now largely corrected back to before the COVID era rally in 2020.

This bearish market is best observed by the lopsided marketplace as an increasing amount of supply has been coupled with a buyers’ strike. This table (attached) shows the ratio of Liv-EX live bids to live offers. In the most liquid segments one year ago, the ratio of bids to offers was largely 1:1. Today the amount of bids to offers has dropped by around 50%.

This lack of equilibrium between buyers and sellers explains the price decreases we have seen in the past 12 months. Conversely, when these ratios begin to trend back to 1:1, prices will have already risen from these lows. The question is have we reached that inflection point or what will trigger that reversal?

Next month, the Bank of England is expected to cut rates, with the U.S. The Federal Reserve expected to follow in September. This begins a period of modest interest rate easing as inflation is now largely under control. Lady Galadriel’s quote is an analogous caution against forgetting the strong correlation between interest rates and Fine Wine prices. In the absence of any additional supply shocks, a reversal of global interest rates and prices at 5 year lows, argues strongly for accumulating Fine Wine now at current levels.

5.25->5% doesnt even remotely equate to the 0.25% era a few years ago. I think there is a long, long way to fall before wine as an investable gets interesting to those who are likely to make that sort of investment. Not least, some of the systematic issues - such as much higher cost of production with inflation, the chronic lack of demand, etc.

I will, somewhat ironically, coin a phrase from jeff leve - buy wine you’re willing to drink at a price you’re happy to pay for it.

But systematic investment into wine, right now, no. I dont know how much further there is to fall, it might be around bottom, but I dont think the returns on the way back up will justify the ivnestments in a 5% world. Even in a 3% world.

To be honest, they didnt even particularly justify it in a 0.25% world.

just to add to that, i think the serious headwinds that companies like Cult and Vinovest are running into now is also likely to kill a lot of the ‘investment appetite’ from non-wine-enthusiasts - which is a good thing imho. Snake oil scam artists.

I saw one portfolio from one of the above which included like 600 bottles of prosseco as ‘investment wine’.

Another example where, if the FCA/SEC would be involved, people should be goign to prison.

I do not want to comment on other companies by name. However i am generally appalled at how the word investment is batted around the wine market. I worked in EM Fixed Income for 20 years, and some of the “recommendations” i see hitting my inbox would be criminal in my former career. I hear what you say about fair value and the headwinds to the market, but i still see more people looking to buy than sell and our company is speficially set up for the latter.

Data? Not even close from what I’ve seen. The correction has been fairly flat with a mild decline in the 20% range, if that, while prices doubled or more during the COVID rally. I haven’t seen a single top wine that I’ve bought or been interested in offered or sold anywhere for anywhere close to the same 2020 price.

I cover biotech and frankly I have been shocked at how directly correlated interest rates have been to sector performance. Even on a daily basis. I guess what we have learned in the recent past is that when you can make 5+% risk free for doing nothing it really makes other risky investments look a lot less appealing. This holds true for biotech stocks, cars, watches, wine etc.

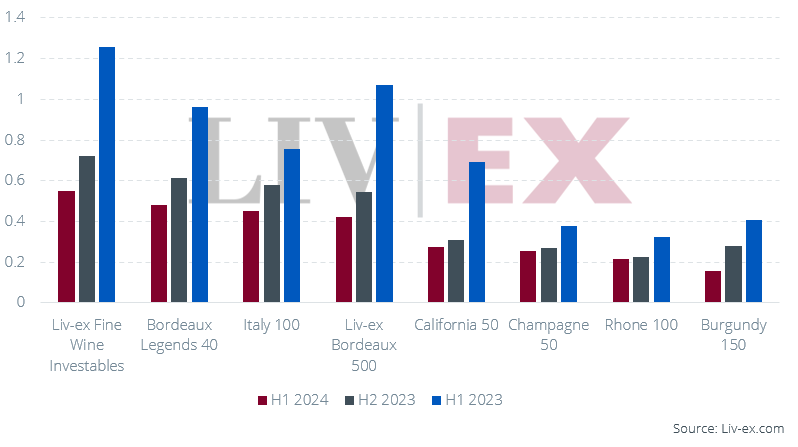

I am looking at the Liv-EX index of Wine Investibles that is in the not I published, you can see it represented graphically. Clearly Bdx didn’t rally as much as Champagne and Burgundy, but in a lot of these wines, they have retraced a lot of those gains.

I also think there is a lot of trading happening at lower levels, but listed prices not so much. Romanee Conti is a bellwether, pre pandemic trading aroudn £13-£14k, and right now its offered almost at those levels again. That is not a one off, Raveneau was another producer that rocketed, 1er Cru’s going from £200 a bottle to over £600… those same 1er Cru’s now offered at £350 if not lower

almost anyone in the business has a vested interest

critics need to keep their writing relevant and marketable (read - high) or else they’ll fade away and lose subscribers, lose access to chateau, etc

the merchants who push EP heavily tell you EP is amazing

the merchants who dont make a lot of money EP tell you to hang on until the wines are physical and to buy back vintages instead

the chateau tell you the wine is unprecedented

sometimes feels like you’re bent over the table and everyone gets to take a turn

and then everyone complains when you dont spend

sweeping generalisations,o f course, just an amused and flippant remark

I cannot think of an product where people love to talk about it so much… all aspects. For just fermented grape juice, it punches well above its weight in capturing people’s imagination

To be fair to @MStarr , he hasn’t recommended a buy. In fact, his first post on the thread was how appalled he was at the application of the word “investment” to wine purchases. He then also made a claim that much of the recent price absurdities have retraced — a claim that might be observable in some categories or specific wines, but unlikely to be generally true. But he didn’t really make a universal claim, and it was more like “the water’s sorta safe” rather than “jump in everybody!” Finally, he simply observed that there were currently more buyers than sellers in the broker market, which I can’t verify and am a little surprised by. You’ve inspired me to contrast his business pitch v one of the “wine investment “ platforms as a kind of PSA for non-financial people as to what should really set off your alarm bells (spoiler, Winebourse comes off much better in the face off - and I am neither a client of nor an investor in any of these companies).

My own 2 cents on whether the market has bottomed:

Minor drops in interest rates will have a noticeable effect on pricing of efficient asset markets. Wine is not one of those markets, at least not in the luxury wine segment. You are unlikely to see a return to the price height of zero-rate markets any time soon. In other words, even if the market has bottomed, the upside is limited in this rate environment.

The market for luxury wines has not cleared to my (imperfect) observations. A lot of retailers are trying to hawk wines at minor discounts to the all time high price when actual auction prices (even including buyer premium) are often substantially lower.

If you don’t believe point 2, I offer the incomplete success of Bordeaux EP 2023 as an adjacent market illustration. Not the same thing, of course, but more evidence of overall market overhang.

Retail offerings that would have disappeared in hours a couple of years ago now just linger, and often get re-pushed by retailers a week or a month later.

When I look at the above, I would conclude that a handful of wines have hit bottom, more because of scarcity premium than overall market conditions. They are unlikely to be representative of the market as a whole. At the same time, the retracement that’s already occurred could mean that the amount of further retracement is limited. As imperfect a guide as this is, I use the 2019 bordeaux EP Covid panic pricing as a baseline for what to expect: the Bordelais offered a roughly 30% discount IIRC for the end the world. You’re unlikely to see a bigger retracement than that from here as rates go down.

And just because decades in finance have made CYA a reflex: the above is not a recommendation or solicitation to buy or sell.

I have not been recommending people to invest in wine since I started my business in 2014. i do recommend on best practises for people who are investing or are collectors so they do not make loss making mistakes when they start on their journey like i did.

This is an extraordinary couple years, with some very big retracement in pricing across the market. Some like HenryB argue it is too little, but from my experience in investment world, bear markets in asset classes are rarely extending beyond 2 or 3 years. I think we are at levels which technically were former support and can now be resistance levels.

Also… i could be wrong. My business has no inventory, we are a stock exchange. Does not matter to me if prices go up or down, although bull markets have more turnover of course. What I post I think is relevant and without any conflicts of interest. I just find the more you discuss with people, the more you learn

I generally agree with your comments about bear markets and the typical doom and gloom of a market is quickly changed in two years when everything goes on a bull run

I’m just not convinced that’s as translateable to wine as it is on equities for example

I have no doubt though in the long term wine prices will go up - inflation guarantees it basically - but I think the systematic weak demand may mean that there may need to be radical things like significant reduction in high end wine production.

With regards to the bottom, on wineEP, we see significantly below right-now market prices on things like BBX. There are sellers for many wines still at say 40% below market, which to me feels like there may still be some way to fall. I don’t expect “market price” to notionally drop (eg widespread) 40%, but I think a smart hunter will find some great deals for a while.

Thank you for the kind words… let me clarify something that i should have written better:

“Finally, he simply observed that there were currently more buyers than sellers in the broker market, which I can’t verify and am a little surprised by.”

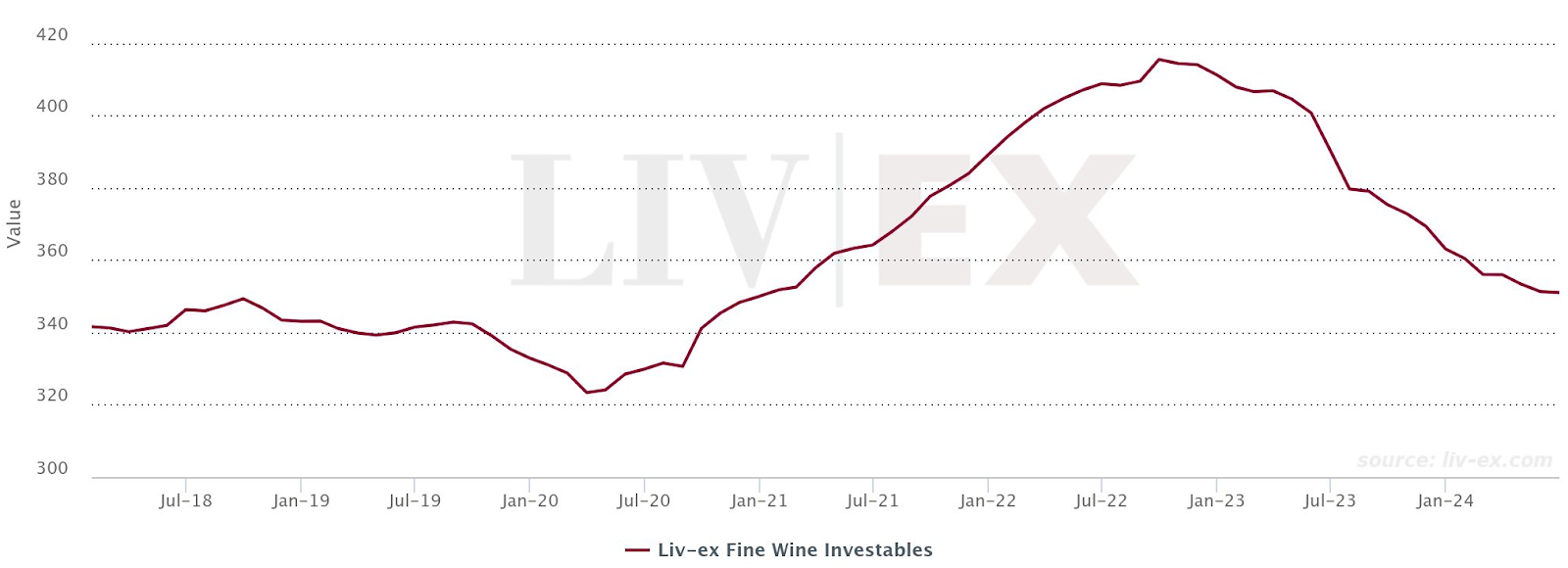

I am sorry that i didn’t write this more clearly. I am talking about individuals, private buyers. The entire market is offered for sure, the graph on my opening part of this chain shows that. However, this is from the wine trade, who i feel is selling off holdings aggressively to either fund losses or working capital. I think its well known that En Primeur is a working capital exercise for many merchants (we do not do EP by the way). They collect money from individual buyers within a month, and they get financing terms for 6-12 months. Disastrous campaigns like 2023 inadvertantly have an impact on the wine trade’s working capital.

I’ll take that in a positive sense rather than apathy

I would say, BBR must be making a packet in this market. Some of the bargains people at wineEP have been sharing are insane - 2021 figeac at like 600/6 (GBP IB). And well below ““market price””